South-east Asia energy shock forces painful policy triage

South-east Asia energy shock is pushing Indonesia and other importers into rate rises, reserve defence and subsidy triage as oil costs bite.

South-east Asia’s oil-poor economies are moving from shock absorption to triage as the Iran war keeps energy costs high, forcing governments to choose between protecting households, defending currencies and preserving growth. What began as a Gulf supply crisis is now arriving in Jakarta and Manila as an emerging-market squeeze: higher import bills, weaker exchange rates and rising pressure on prices that central banks cannot easily look through.

The story is no longer only about crude. In fuel-importing economies across the region, the shock is running through three channels at once: the cost of buying oil, the cost of defending local currencies against a stronger dollar, and the fiscal cost of cushioning voters from dearer transport and electricity. Every response, from rate rises to subsidies, eases one strain while deepening another. As the Financial Times reported on regional countermeasures, south-east Asian governments are no longer waiting for a clean external fix; they are rationing policy room.

Officials are reading the same evidence through different lenses. Households and transport firms feel the shock first at the pump; currency traders read it in reserve losses and bond yields; central banks worry that a temporary supply disruption is hardening into an inflation regime. International Energy Agency chief Fatih Birol has warned that the market may be entering a “red zone” by mid-summer, and even a diplomatic breakthrough would not quickly repair the damage already done to importers’ balance sheets.

A balance-of-payments shock

The core vulnerability is mechanical. Roughly 20 per cent of the world’s oil and liquefied natural gas passes through the Strait of Hormuz, and about 80 per cent of the oil shipped through the choke point is bought by Asia. Even after an IEA-coordinated release of 400 million barrels from strategic reserves, the region remains exposed because no hedge can erase the macro effects of a long spell of expensive energy.

This is a balance-of-payments story as much as a commodity one. Higher crude prices widen current-account pressure in economies that import most of their fuel, while the stronger dollar raises the local-currency cost of each barrel again. Bloomberg Markets described the weakest Asian economies as facing simultaneous pressure to tighten policy even as the growth hit deepens. The New York Times noted that the foreign-exchange buffers many Asian countries built after the 1997 crisis are being tested again, which helps explain why reserve defence has become as important as headline inflation.

Trade and FX data already show the damage. Reuters’ energy reporting said Asia’s oil imports in April fell 30 per cent from a year earlier to their lowest since October 2015, a contraction that suggests demand destruction is beginning before governments have restored confidence. Lower imports do not solve the problem. If refiners and buyers are already scaling back to that degree, the region is not solving the shock; it is transmitting it into slower activity.

As Reuters’ Asia currencies analysis shows, the next step is plain: once oil prices and the dollar rise together, rate policy becomes defensive, not growth-supportive.

“How many hikes does it really take to incentivise capital to come in? The answer could be quite a lot.”

— Navin Saigal, quoted by Reuters

Saigal’s point matters because higher rates are only a partial answer for energy importers. Tightening can slow capital flight and support the exchange rate, but it also raises borrowing costs for businesses that are already paying more for fuel and freight. That is the regional bind in one sentence.

Indonesia as test case

Those trade-offs are clearest in Indonesia. The rupiah has fallen 12 per cent against the dollar under President Prabowo Subianto, and Bank Indonesia surprised markets with a half-point rate increase after the currency hit successive record lows. A follow-up Bloomberg report suggested analysts expect more tightening, even though further hikes may still fail to prevent more losses in Indonesian assets.

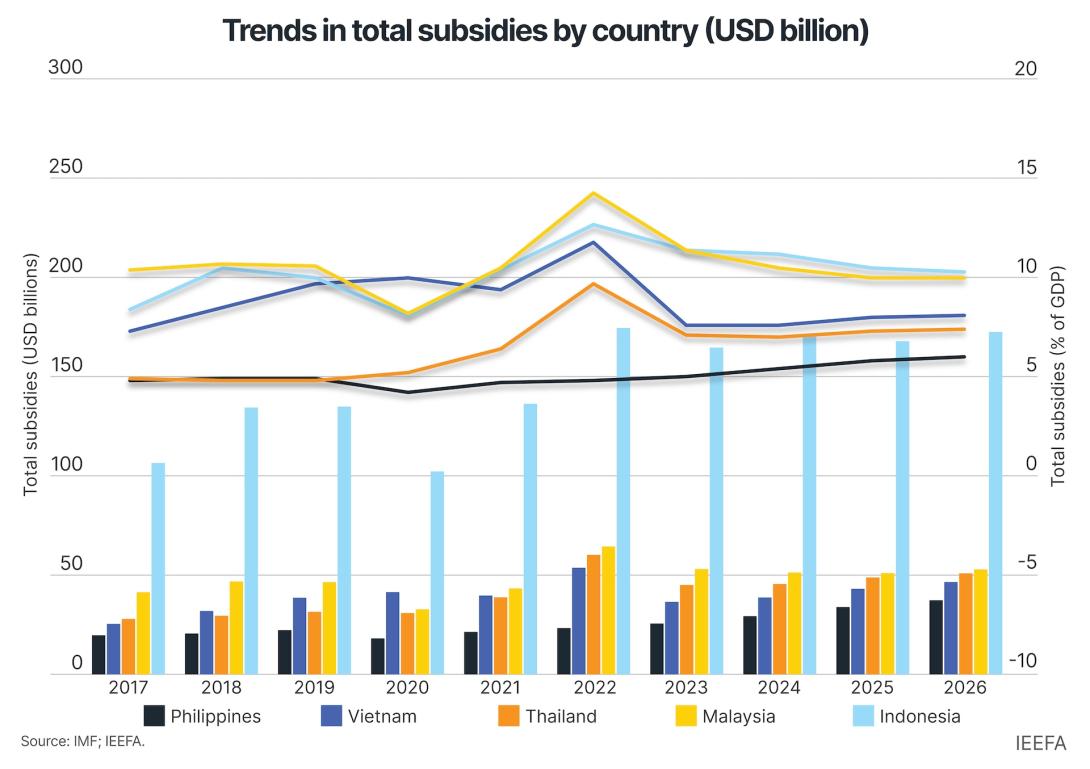

For households, the shock is less technical than it appears on a central-bank dashboard. Costlier imported fuel feeds through to bus fares, power bills and food distribution costs, while weaker currencies make each new shipment more expensive in local terms. That is why subsidy policy sits alongside rate policy in this story. Governments can soften the blow for consumers, but each intervention eats into fiscal room that may be needed if oil stays high through the northern hemisphere summer.

No single lane is cost-free. If officials lean harder on interest rates and reserve sales, they risk a sharper domestic slowdown. If they lean harder on subsidies, they shift the strain to the budget and encourage heavier fuel use when the region needs demand to adjust. If they do too little of either, the currency may absorb the shock anyway. The real debate is no longer whether authorities act, but which pain they prefer to own.

Across the region, the burden is uneven, though not in a comforting way. Bloomberg’s broader read on emerging Asian stress and Reuters’ regional survey both point to countries with weaker external balances and heavier import dependence as the first to feel the squeeze. The Philippines belongs in that conversation; India does too, even if it sits outside south-east Asia proper. The comparison matters because it shows the shock is not evenly Asian. It is concentrated in the countries with the least room to subsidise fuel, absorb currency losses or keep hiking without bruising growth.

“The biggest pain of this crisis will be felt in developing Asia and Africa.”

— Fatih Birol, International Energy Agency, via CNBC

Birol’s warning is easy to read as a commodity-market line. It is better read as a fiscal one. Developing importers do not simply pay more for oil; they pay more for electricity generation, transport, food distribution and every subsidy meant to soften those blows.

Why the pain will linger

A reopening of Hormuz would not undo the policy tightening already under way. The question for central bankers is whether the shock stays in energy or leaks into expectations. In Australia, RBA assistant governor Sarah Hunter warned that recent oil-price moves risk unanchoring inflation expectations. That concern travels easily across the region, because once firms assume higher fuel costs will stick, they begin passing them through more aggressively.

Stress is showing up elsewhere too. CNBC reported that Japan and China were among foreign governments retreating from U.S. Treasurys as Gulf war fallout rattled Asian currencies. The mechanics differ by country, but the signal is the same: authorities are preserving liquidity and defending domestic stability first, even if that means giving up some room elsewhere in their portfolios. That is not a panic trade. It is a reminder that the oil shock is reaching balance sheets, not just fuel invoices.

Another problem is sequencing. Diplomatic headlines can move crude lower quickly, but governments cannot instantly roll back emergency measures once they have hiked rates, run down reserves or expanded subsidies. NPR’s reporting on negotiations over the Strait of Hormuz underscored how unclear the details remain despite President Donald Trump’s claims of a breakthrough. For south-east Asia’s importers, that uncertainty matters almost as much as the oil price itself. Policy has to be set on what officials can verify, not on what markets hope.

South-east Asia’s energy problem now looks less like a short-term supply scare and more like inflation triage. The first question was whether governments could cushion households. The next is whether they can do that without exhausting reserves, locking in higher inflation or choking off growth with too much monetary defence. If the market really does move into the IEA’s red zone, the region will not be choosing between good options. It will be choosing which cost arrives first.

Marcus Holloway

Markets editor covering UK gilts, sterling and the Bank of England. Previously a fixed-income strategist in the City.